INTRODUCTION

As world leaders gather in Sharm al Sheikh for the COP 27 climate summit – Africa’s COP – attention is focused squarely on the continent’s energy future. With discussions on climate financing at the forefront of the agenda, so are the seemingly contradictory policies of Western governments, namely those in Europe. As the developed world reiterates commitments to climate goals over the medium to long term, it is simultaneously grappling with the immediate crisis of meeting its energy demand following Russia’s invasion of Ukraine. Africa’s gas potential is clearly in Europe’s sights – even as the bloc’s leaders push for an accelerated energy transition. Africa is faced with a choice: provide gas for Europe now – with short-term economic gain for Africa – or focus funding on the development of renewable energy sources, with long-term energy security, economic growth and stability, and global climate goals in mind.

Europe’s outreach to Africa as part of its strategy to replace natural gas imports from Russia comes with considerable risks that could ultimately delay African countries’ transition to renewable energy. While the proposal could help Europe achieve energy security over the short to medium term, encouraging investment in natural gas risks actively delaying and even undoing efforts made by African states to deploy clean energy programmes, unless the EU facilitates financing for both. Such efforts also risk heightening further the continent’s vulnerability to climate change, which has already had a devastating effect on Africa’s populations.

European leaders have urged their African counterparts to accelerate their transition to clean energy, though financing costs remain prohibitive as green projects carry high risks. However, wealthy nations have failed to deliver on a long-held pledge to provide poorer countries with annual climate financing of $100 billion per year by 2020.1 Further, following Russia’s invasion of Ukraine, G7 leaders agreed in June to back public financing for natural gas projects,2 including installation of 20 floating liquefied natural gas (FLNG) terminals to receive new volumes of natural gas and convert it to heating fuel for Europe.3 EU countries now need to secure LNG supplies in an already tight market.

Countries including resource-rich African nations are now more likely to find financing for the development of hydrocarbon resources (which had previously become hard to secure) as Europe seeks to fulfil its natural gas demand. Financing such projects would fast-track resource development and aid economic development in Africa.

In fact, it would also align with the sentiment expressed in a technical document prepared by the African Union for an energy ministerial held in June via video-link. The document noted that in the short- to medium-term, fossil fuels, especially natural gas, will have to play a crucial role in expanding modern energy access and accelerating the uptake of renewables.4

While investment in Africa’s hydrocarbons – and the natural gas sector – could be beneficial in the near term, it could also carry considerable risk if resources are developed solely with the goal of meeting European demand. European demand is likely to be short to medium term as EU customers are unwilling to sign typical 15-25 year contracts, given that EU energy policy limits the role of natural gas in the energy mix. Further, gas and renewables projects are likely to compete for the same pools of finance — a prospect that would prove detrimental to the advancement of clean energies.

As long as security of demand is met, natural gas sales provide investors with guaranteed rewards across the supply chain. Conversely, investors in renewable projects are rewarded only if they are engaged in power generation. The financial benefits are less if they are vested in funding grids and energy storage systems in developing markets which are essential pieces of infrastructure for reaching consumers. In other words, investors will be more incentivised to develop gas over renewables projects.

While there might be compelling motivation for gas-rich African countries to develop and export natural gas to Europe, it is important to highlight that doing so will likely be accompanied with time-sensitive risks that could leave states with stranded assets as the world moves to greener forms of energy. Additionally, it carries the risk of undermining advances in developing and expanding clean energy supplies throughout Africa by locking economies into long-term gas infrastructure and contracts. Thus, potential costs for Africa would be extremely high in terms of its development and in relation to climate change risks.

Clean energies help with climate change mitigation and adaptation while presenting opportunities to develop infrastructure compatible with the complex new energy systems and economic models of the future. Renewables also provide affordable, sustainable and reliable electricity, which is at the core of commercial and industrial expansion and economic diversification. Additionally, technologies applied on-premises or through community and mini-grid models reduce risks of supply disruptions, such as those experienced by hydrocarbon producers in Africa due to conflict, terrorism or instability.

With global investors increasingly focused on low-carbon technologies, clean energy projects could attract much-needed financing to Africa. This would be possible if solid and country-specific frameworks are developed, with financial and technical support from international financial institutions to de-risk counterparties and implement bankable projects.

This paper comprises three sections:

- An examination of the current state of play in global gas markets following Russia’s invasion of Ukraine, with Europe moving to diversify and supplement supplies while accelerating its energy transition.

- Considerations surrounding Africa’s gas potential and challenges, as well as the interplay between African gas development and European energy demand.

- Exploration of the impact of climate change on the African continent and how boosting development of clean energies would help Africa achieve economic and energy resilience while contributing to national, regional and global greenhouse gas emissions goals.

EUROPE SEEKS ALTERNATIVES TO RUSSIAN GAS

Russia’s invasion of Ukraine has caused a major dislocation in energy markets. It is not the first time that Moscow’s policy towards Kyiv has left the EU scrambling to find natural gas supplies from alternative sources.5 However, in previous instances, compromises were reached, and Russian gas flowed uninterrupted to customers throughout Europe.

The US and EU’s response to Russia’s aggression,6 which include a series of measures aimed at curtailing Moscow’s oil and gas revenues, has created a structural fault in the European hydrocarbon energy system. Given that the Ukraine war is likely to continue for some time, EU states now face the challenge of replacing Russian gas supplies indefinitely. Despite having spent decades trying to better manage EU dependency on Russian gas, almost all European states, most notably Germany, failed to do so.7 Short-term policies and expediency proved to be a more attractive option than committing major investment to long-term contracts with LNG suppliers and constructing regasification terminals across the continent.

Economic, political and climate challenges have made reducing hydrocarbons in Europe’s energy mix an even more pressing issue which will surely accelerate its journey towards the energy transition. However, the EU’s decision in July to keep some specific uses of natural gas in its taxonomy of sustainable energy sources8 means that its shelf-life as a transition fuel has been extended. Moreover, the EU must source replacement gas from other suppliers to fill the deficit left by Russia, at a time when market conditions have pushed prices to unprecedented levels.9

Efforts to negotiate short- or medium-term contracts with other LNG suppliers such as Qatar have proven difficult. Doha’s insistence on security of demand, which it has already secured with its Asian customers, has made it challenging for European countries such as Germany to negotiate shorter-term contracts,10 especially taking into consideration that the volumes needed are simply not there. As a result, Europe is now turning its attention to natural gas prospects on the African continent to help plug the supply gap over the short to medium term.11

With 17.55 trillion cubic metres (tcm) in gas reserves, Africa holds approximately 9% of global gas reserves,12 and currently accounts for 6% of the world’s total natural gas production. Nigeria, Algeria, and Egypt constitute 85% of the continent’s gas production and are among the top twenty natural gas producers in the world.13 However, African reserves remain largely unexplored, despite significant discoveries in Senegal, Mauritania, Mozambique, as well as Tanzania accounting for almost 40% of global new gas discoveries in the last decade.14 The continent’s potential is well-documented but remains unrealised due to multiple inhibiting factors, including governance issues, high costs and risks related to the political, security and legislative environment.

While African governments may view gas as fuel for meeting domestic power generation demand to enable security and socioeconomic growth, population growth and rapid industrialisation will boost domestic demand across Africa. The continent’s estimated growth forecast of 30% by 2040 is significantly higher than expected global demand growth of 10%.15 Increases in domestic demand have already led states to redirect volumes back home from abroad. For example, Algeria’s capacity to export is somewhat compromised as its market consumes some 60% of gas output,16 predominantly in the residential sector and in gas-powered plants which provide the country’s electricity.17 However, African oil- and gas-producing states are heavily reliant on export revenues and their leaders are confronted with the dilemma of either meeting local demand or generating national income.

At the same time, Europe’s desire for African gas has increased following Russia’s invasion of Ukraine. Italy has held exploratory discussions with Congo and Angola and is seeking to ramp up imports from Egypt, while the Italian energy group ENI hopes to expedite LNG production at its floating gas facility in Mozambique before the end of 2022.18 Germany is in discussions with Senegal about future supplies, the EU signed an MoU with Egypt and Israel regarding future imports, and the European Commission dispatched its Deputy Director-General for Energy to Nigeria for talks on increasing gas provision from the West African country.19 With gas prices soaring, the prospect of securing higher revenues over the long-term is already causing exporting countries in Africa to adjust their priorities. For example, in 2022, Egypt made plans to divert 15% of gas used for domestic electricity generation to exports to boost its struggling economy.20

The loss of Russian gas from European markets presents Africa with an opportunity for its “gas moment”. The European Commission’s REPowerEU package,21 published in May, outlines its plans to wean Europe off Russian gas before 2030. Its measures include diversifying suppliers, securing a short-term injection of gas and growing its renewable energy industry. Africa’s gas potential, therefore, looks appealing to EU leaders as it could help satiate Europe’s short- to medium-term gas requirement while revitalising Africa’s natural gas industry and boosting its economies.

Europe needs to replace just over 100bcm/yr of Russian gas by 2030 in order to meet its Fit for 55 and REPowerEU objectives.22 Several measures have been proposed to achieve this, one of which is obtaining an additional 50bcm of LNG imports and 10+bcm of pipeline gas.23 Under REPowerEU, Europe also aims to reduce gas consumption by 52% by 2030 in parallel with substituting hydrocarbons for clean energy sources.24 This timeframe leaves new gas suppliers only eight years to come onstream; projects typically require several years’ lead-time before production can begin, and a lifespan of at least 20-25 years to achieve economic viability. Ensuring security of demand, therefore, is critical for investors and operators.

PRODUCTION TRENDS AND CHALLENGES IN AFRICA

Existing suppliers such as Nigeria, Angola and Algeria, or those on the cusp of beginning production, could feasibly increase output in the near-term, provided they receive sufficient financing. But short-term contracts may not benefit African states, which would need to allocate and invest substantial public financial resources to de-risk projects in order to secure partial funding and market share. In parallel, the EU has signed an agreement with the US for an additional 50bcm of LNG per year until at least 2030.25 Despite the REPowerEU package specifically mentioning untapped potential in sub-Saharan Africa,26 Europe may not actually need significant new volumes of African gas, especially if the US delivers on its contractual obligations and the EU implements other elements of its energy strategy.27 Europe is working with a short-term fix mindset, whereas Africa needs long-term financial and energy sustainability. Since it is not clear how long the hydrocarbon market will last, there is a significant risk of leaving African producers with stranded assets.

This uncertainty adds to the numerous challenges already facing Africa’s oil and gas industry, including political instability, significant security risks, high project costs, and a lack of infrastructure. These have lowered the continent’s appeal as an investment destination in the past and may deter major investors once again.

Libya provides an example of an African state whose considerable gas potential has been held back by political instability. The country has suffered from civil war, militia violence and foreign intervention for over a decade, and now has two rival governments and faces factional competition over hydrocarbons facilities and revenues.

In 2021, TotalEnergies halted the construction of its $20bn Mozambique LNG project, citing an Islamist insurgency in the country,28 and resulting in delaying 12.9 million tonnes per annum (Mtpa) of gas coming onto global markets while postponing the possibility of adding a further 10mtpa during the project’s next phase. TotalEnergies’ force majeure declaration has also had an impact on ENI’s Rovuma LNG project, which will share the same site and some of the same facilities. The Italian major has postponed reaching its Final Investment Decision (FID) until TotalEnergies lifts its force majeure, putting on hold another 15.2mtpa of LNG.29

On average,African oil and gas assets are 15-20% more expensive to develop and operate than in other parts of the world.30 Political and security challenges have harmed project development, slowed the building of infrastructure, and added a premium to project financials. As a result, Africa suffers from limited national and regional pipeline infrastructure and has limited connectivity with Europe. This has hindered African gas development, domestic distribution and export potential to date.

Efforts to improve Africa’s pipeline infrastructure have made little progress given the challenging operating environment. The planned Trans-Sahara Gas Pipeline (TSGP), which runs over 4000km from Nigeria to Algeria and Morocco, has been hampered by long-running security issues, including intercommunal conflict, the threat of Boko Haram in Nigeria, and extremist activity in Niger and Algeria. It also comes with a prohibitively high price tag of approximately $13bn,31 underscoring the project’s financing challenges. Despite Algeria, Niger, and Nigeria’s signing in July of an MoU reaffirming commitment to delivering the project, widespread theft, corruption and governance issues in those countries will continue to challenge its development.32 The pipeline is designed to carry 30bcm/year upon completion, but no progress of note has been made on its development since its inception 40 years ago.

Similar challenges have prevented progress on an offshore Nigeria-Morocco gas pipeline, although recent statements indicate the parties hope to reach FID next year.33 The pipeline was conceptualised in 2016but movement on its development has only picked up now that gas demand and prices arehigh. A September 2022 MoU reiterated stakeholders’ commitment to the project’s feasibility study.34 Further, the Islamic Development Bank and the OPEC Fund for International Development – along with the Nigerian and Moroccan governments – recently contributed $14.3m to the second phase of the Front-End Engineering Design (FEED) project.

Designed to cross 13 African countries over 5600km with an estimated development cost of $20m-$25bln, the Nigeria-Morocco gas link would be the world’s longest offshore pipeline. It would supply landlocked Niger, Burkina Faso and Mali en route to delivering gas to Morocco for connection into the Maghreb Europe Gas Pipeline (MEGP) and on to the European gas network.35 However, construction will take at least eight years,36 by which point the EU will likely have already diversified its gas supplies, reduced consumption and accelerated the development of renewable energy sources. This suggests Europe may not have a need for MEGP gas by the time it comes onstream.

Compounding such challenges is the fact that African gas reserves are estimated to be 70%-80% more carbon-intensive than other assets around the world. Over 30% of Africa’s gas production is associated gas, meaning it is a by-product of crude production and therefore directly linked to the oil industry.37 As investors reduce their exposure to oil projects and global investment in hydrocarbons shrinks, African projects are expected to become even more costly—and therefore, even less competitive. Energy companies will prioritise lower-emission basins with greater short-term potential, meaning African exploration and production projects will become less attractive. The risk of stranded assets therefore rises, and much of the continent’s extensive gas reserves will remain undeveloped.

Africa’s current greenhouse gas (GHG) emissions are low, comprising only 3% of global emissions. In a recent report, the IEA argued that if Africa were to exploit all its gas resources, its contribution to global emissions would only rise by 0.5% – to 3.5% – by 2050.38 The report stated that Africa could achieve universal energy access by 2030 with $25bn/yr in investment — the equivalent of just 1% of funds that pour into the global energy sector annually.39

AFRICA’S CLIMATE CHANGE RISKS STRENGTHEN CASE FOR RENEWABLES

While Africa’s emissions constitute the smallest share of global GHG emissions, compared to 23% for China and 19% for the United States,40 the continent is the most vulnerable to climate change in all scenarios where global warming exceeds 1.5 degrees Celsius.41 Climate change is a threat and vulnerability multiplier, and the continent is already feeling its impacts through extreme weather, food and water insecurity, and associated economic and fiscal costs. Climate change increases fiscal sustainability risks especially in highly indebted countries such as those in Africa.

Failure to mitigate the impact of climate change will reverse progress in poverty alleviation and economic growth, thereby impeding development. By 2030, 10% of Africa’s population, or 180 million of the most vulnerable, will be exposed to drought, floods and extreme heat.42 The cost to the economy will also be significant, potentially wiping out almost 10%-13% of the continent’s43 gross domestic product (GDP),44 with the lowest-income nations experiencing the largest fiscal deficit.

The total cost of climate adaptation and mitigation, including losses and damages, is estimated at $2.8 trillion within this decade. In Africa, climate financing needs are highest in Southern and Eastern African countries,45 and investment in adaptation measures alone would cost 2-3% of the continent‘s GDP.46

Renewable energy is critical to help mitigate the impact of climate change and compensate for current energy models that have failed to provide equitable electricity access and inclusive economic growth.

Clean energy presents an opportunity to provide the African continent, despite its wide disparities, with a just and secure energy provision. Emphasizing clean technologies would allow African states to expand commercial and industrial sectors in Africa through reliable and affordable energy supplies and attract investment to grow their economies and create new employment opportunities. Building inclusive energy systems that place people at the centre of policymaking, and account for the needs of the complex power systems and economies of the future, will help transform African economies.

As global electricity access increases, large disparities have emerged in the pace and pattern of electrification. The world is not on track to ensure access for all to sustainable, affordable, and modern energy by 2030.47 For Africa, the disparities are clear. North Africa is fully electrified, but the share of electrification in Sub-Saharan Africa was only 46% in 2021.48

Despite Africa’s urban communities enjoying widespread access to electricity, with overall access doubling from 2013-22 (supplying 75% of households), 35% of households in rural areas remain without electricity.49 As such, some 600 million people on the continent do not have electricity, making up two-thirds of people lacking such access globally. The rate of electrification slowed during the COVID-19 pandemic, pushing 40% of African countries into financial distress and reversing progress in increasing electricity access.50 On the economic front, 83% of African countries are dependent on commodity exports.51 However, despite the benefits that export-led growth has delivered, notably during commodity super-cycles, it has not always resulted in more inclusive development. Overreliance on commodities and poor economic diversification has led other business sectors to produce low value-added goods and achieve low productivity levels. Expanding Africa’s service and industrial sectors is essential for diversifying the continent’s economies, increasing productivity and creating jobs,52 but these sectors require reliable, affordable and sustainable access to energy.

A glimpse into the energy sector shows that the dominant model is utility-scale, centralised and heavily reliant on fossil fuel-powered plants. These systems have failed to meet the energy needs of the population because the provision of electricity has been carried out only by public monopolies with limited private sector and local community engagement and has favoured urban populations and large industrial consumers. However, renewable energy can be deployed through numerous models, including community solar photovoltaic and mini-grid models that would engage a multitude of stakeholders and emphasize the needs of the local community.

Whereas gas production and supply are vulnerable to conflict, criminality, insurgency or logistical disruption, renewable energy deployment options, such as mini or micro-grids and on-premise generation, significantly reduce these risks and increase security of supply.

Clean energy is an important climate mitigation-adaptation measure that enables the construction of new, modernised infrastructure, potentially attracting investment to the continent as financiers move away from long-term fossil fuel investments. In the past decade, investments in renewable energy in Africa comprised only 2.4% of global renewable energy investments.53 There were large disparities between countries, with Egypt and Morocco recording more investment than other African nations. Although insignificant on a global scale, the current share of investments constitutes three-fold growth from a decade earlier, and the potential for further growth is substantive. A solid framework centred around the energy transition could increase investment in Africa, driving GDP growth to 7.5% in the first decade and 6.4% in the following decades through 2050.54 Such a framework entails: 1) increasing public spending in renewable energy and mostly power grids and flexibility systems that are more difficult to secure private investments for compared to generation, 2) building an enabling business environment and investment climate to engage the private sector, 3) adopting policies and regulations in favour of low-carbon technologies, 4) providing fiscal incentives, and 5) building and strengthening relevant institutions.

The versatility of renewable energy requires country-specific models and accounting for integration systems. There is not a single solution for all African countries, but energy policymaking and implementation should account for the complex energy systems and economic models of the future. Africa’s countries vary in terms of clean energy sources, renewable energy technology, deployment models and infrastructure requirements. They also differ in terms of required storage and flexibility systems, depending on the level of integration of variable renewable energy into the grid.

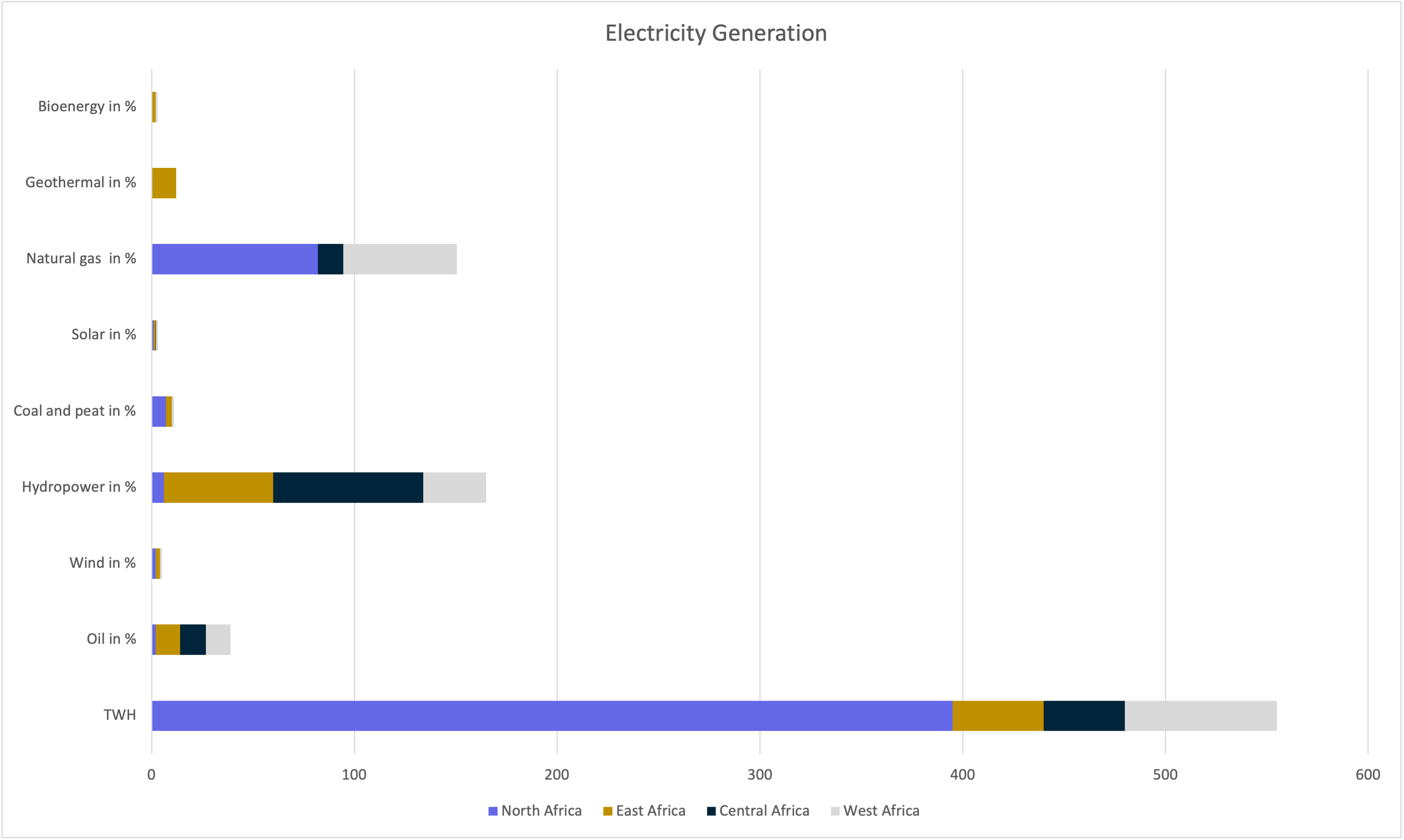

Hydropower and geothermal power could help meet baseload demand, but these renewables sources are not available at a large scale in all African countries. Ethiopia has 658.6MW of hydropower in its Gilgel Gibe III plant, and Uganda is home to the 183.2MW Isimba hydropower plant. Meanwhile in West Africa, Ghana has the 400 MW Bui plant, Guinea hosts the commissioned 240MW Kaléta plant, and Cote D’Ivoire has its 275MW Soubré plant. In Central Africa, hydropower constitutes 65% of power generation capacity.55 But this generation capacity and potential future expansions in hydropower are at risk due to climate change-induceddrought and flooding. Developing other renewable energy sources and creating storage capacity is essential for the future.

In addition to hydropower plants, East Africa holds geothermal power, specifically in Kenya. Kenya is at the forefront of clean energy, having achieved over 80% of power generation through renewables.56 The country possesses the world’s lowest-cost geothermal powerplant with a combined installed capacity of 558.4MW, and Africa’s largest wind power plant of 310MW in Lake Turkana. However, the region is highly dependent on biomass due to low electricity and clean cooking access.

North African countries make up the continent’s biggest energy market. But they also hold Africa’s lowest share of renewable energy in the power mix, with natural gas being the dominant source of power generation. Regional power demand is increasing at an unsustainable rate, prompting a focus on alternatives, especially among oil and gas producers seeking to free up gas for export. Solar and wind farms have dominated renewable energy projects in the region and are expected to experience significant growth, with ambitious targets pledged by governments. Among North African countries, Morocco is leading in renewable energy deployment with a major focus on concentrated solar power (CSP) in the Ouarzazate farms, which benefit from molten salt storage. Egypt is increasing focus on solar photovoltaic with the landmark 1.5GW Benban mega-project.

In Nigeria, Africa’s largest economy and a major oil and gas producer, only 55% of the population has basic electricity access. In 2019, only 15% of West Africa’s population had access to modern clean cooking fuels, even though gas is produced in the region and forms the dominant source of power generation. Most of the population still relies on traditional biomass for cooking. Meanwhile, Central Africa has the continent’s lowest access to energy, with 32% access to electricity and 17% access to clean cooking fuels.57 The Democratic Republic of Congo is second to Nigeria in hosting the largest population without electricity access.

Beyond providing access to basic energy needs, growing the economy and meeting future sector digitisation and electrification requires sustainable energy models. These models will need to be country-specific, as African countries vary in their renewable resource potential and attractiveness to investors.

Innovative financing and technical packages are needed to scale-up renewables, including building bankable projects and de-risking off-takers. The support of international financial institutions is key in this regard. Scaling-up renewable energy investments in Africa requires stepped-up financial commitments from the international community, but other measures are also needed.

Blended finance, grants for strategic projects and efficient public-private partnerships are at the core of securing financing for the capital-intensive clean energy industry. Additionally, technical support for the counterparty is critical to achieving bankable projects. Most countries would require assistance with de-risking renewable energy projects and building a bankable counterparty.

Energy infrastructure projects should undergo socio-environmental impact assessments that would identify strategies to mitigate any potential risks on livelihoods and the environment. Building energy infrastructure that contributes to sustainable and economic development goals reduces potential impacts on human security, economic turmoil and instability. The alternative is depriving entire populations of benefiting from the industries of the future.

CONCLUSION

On the surface, exploiting Africa’s natural gas potential would appear to provide quick wins for both Europe and Africa. But it would fail to help deliver long-term energy security, economic prosperity and stability for Africa. The European Union’s need to make up for lost Russian gas supplies has pushed it to engage with African governments, but the bloc’s objectives are short-term and conflict with African project timelines and development goals. Africa faces the risk of having stranded assets and locking itself into long-term infrastructure financing commitments that would undermine advances in developing and expanding clean energy provision across the continent.

One way to remedy such risks is to further invest in clean energy as it presents an opportunity to provide Africa with a just and secure energy provision, despite the continent’s wide disparities. Emphasizing clean technologies would allow African states to expand their commercial and industrial sectors through reliable and affordable energy supply. It would also help attract investment, create much-needed employment and grow Africa’s economies. Renewables would provide affordable, sustainable and reliable electricity, which is at the core of industrial expansion and economic diversification.

Transforming African economies requires building inclusive energy systems that place people at the centre of policymaking and account for the needs of the complex power systems and economies of the future. The EU, along with development and climate financing institutions, can look to prioritise meeting long-term, net-zero objectives and support the development of clean energy across the African continent. Funding green energy technology would not only assist in climate change mitigation and adaptation but would also allow Africa to develop infrastructure that serves its economies and populations as the world pushes towards a post-hydrocarbon future.

References

1. Weise, Zia (2022), “Rich countries broke climate finance promise, says OECD”, Politico, 29 July.

2. Castle, Almu (2022), “G7 disappoints with fossil fuel ‘loophole’,” France 24, 28 June.

3. (2022), Europe Plan for Floating Gas Terminals Raises Climate Fears,” Bloomberg, 31 August.

6. (2022), “United with Ukraine,” 21 October 2022 “EU response to Russia’s invasion of Ukraine,” European Council.

20. Reuters (2022), ”Egypt to ration electricity to boost gas exports”, 12 August.

21. European Commission (2022), ”REPowerEU Plan”, 18 May.

26. European Commission (2022), ”REPowerEU Plan”, 18 May.

28. Jucca, Lisa, (2022), ”Africa is imperfect solution to Europe’s gas woes”, Reuters, 28 April.

32. Africa News (2022), ”Nigeria-Morocco gas pipeline project takes off”, 16 September.

35. Africa News (2022), ”Nigeria-Morocco gas pipeline project takes off”, 16 September.

41. African Development Bank Group. ”COP 25: Climate Change in Africa”.

42. World Meteorological Organisation (2021). ”State of the Climate in Africa 2020”.

44. African Development Bank (2019). ”Climate Change Impacts on Africa’s Economic Growth”.

47. SE4All (2022). ”Tracking SDG7: The Energy Progress Report 2022”.

48. SE4All (2021). ”Tracking SDG7: The Energy Progress Report 2021”.

50. International Energy Agency (2022). ”Africa Energy Outlook 2022”.

54. IRENA (2022). ”Renewable Energy Market Analysis: Africa and its Regions”.

57. IRENA (2022). ”Renewable Energy Market Analysis: Africa and its Regions”.